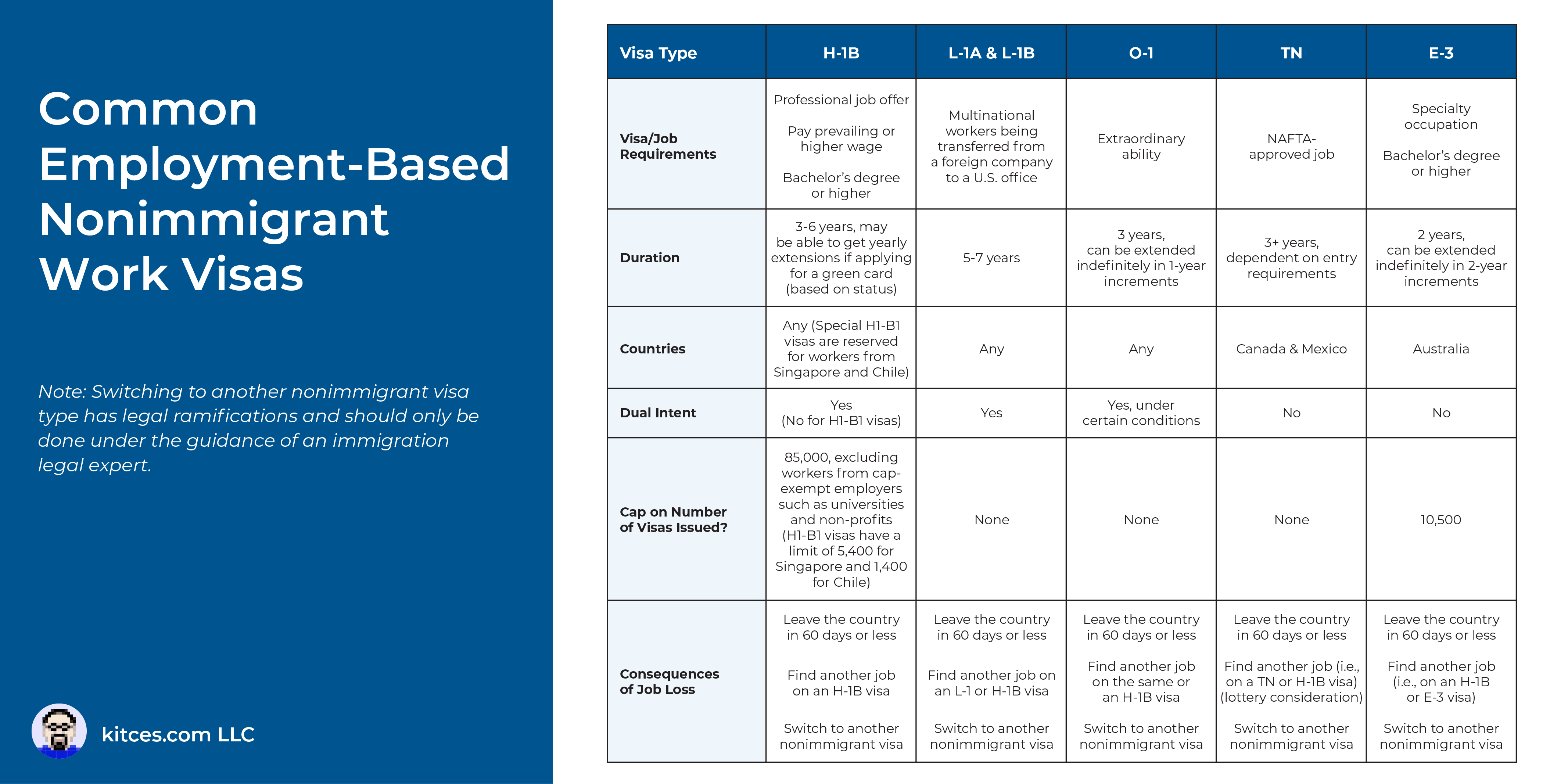

Amid a good job market and low unemployment charges, a big quantity of the U.S. ‘expertise hole’ is crammed by foreign-born staff on employment visas just like the H-1B. These visas enable international staff to stay and work within the nation briefly whereas they’re employed – though in observe, this may imply that people can spend years or a long time (and even their whole profession) working within the U.S. on a ‘short-term’ visa.

Like native-born staff, international staff want to consider saving for retirement, planning for his or her kids’s school, managing healthcare prices, and all method of different monetary targets. Nonetheless, the system within the U.S. that incentivizes saving for these targets for Americans – specifically with tax-advantaged accounts comparable to 401(ok) plans, IRAs, 529 school financial savings plans, and Well being Financial savings Accounts (HSAs) – can impose hurdles on international nationals who depend on them for their very own financial savings wants.

For instance, the tax advantages of sure accounts can typically work within the different path if a non-U.S.-born employee contributing to them finally strikes again to their residence nation. Roth IRAs, as an example, are taxed as soon as upon contribution and may develop tax-free thereafter within the U.S., which might enable for a big accumulation of tax-free financial savings over time; nevertheless, as a result of some nations don’t acknowledge the tax-free nature of Roth accounts, withdrawing from the IRA in a foreign country later might trigger it to be taxed a second time, eliminating the first advantage of Roth financial savings.

Moreover, international staff usually additionally face hurdles in opening and accessing some accounts. For instance, some brokerage corporations gained’t even enable international nationals to open new accounts, and others might require the person to shut the account and transfer their belongings out in the event that they ever transfer away from the U.S. and in some instances, whole account varieties could also be unavailable as a result of employee’s international standing, comparable to 529 plans, which require beneficiaries to have a U.S. Social Safety Quantity (making them successfully off-limits to people with noncitizen dependents) and necessitate a distinct method to school financial savings than is widespread for U.S. residents.

Finally, navigating saving and investing for foreign-born staff requires a cautious stability of understanding the concerns and potential pitfalls of various financial savings methods, figuring out the individual’s targets and plans (together with potential relocation abroad), and – maybe most significantly, given the uncertainty that may include staying within the U.S. on a piece visa – sustaining sufficient flexibility to protect their belongings ought to these plans change. Advisors who can keep on high of modifications to immigration and tax regulation and assist with navigating these challenges can serve a helpful function for international nationwide purchasers – a possible consumer base that’s solely poised to develop in an more and more international workforce!

![]()

{kind=link}