Globally, the rising youth inhabitants presents a possible for financial progress. Nonetheless, youth in creating nations additionally nonetheless face boundaries to entry monetary providers, reminiscent of three of 10 million Cambodian younger adults who stay financially underserved.

Youth financial savings, specifically, has immense potential for enhancing a rustic’s gross financial savings fee, asset-building and instilling wholesome monetary habits in prospects. At Girls’s World Banking (WWB), now we have seen repeatedly the social and monetary returns for monetary service suppliers that acknowledge this chance.

In Cambodia, WWB and AMK Microfinance Establishment designed and piloted options to drive younger grownup buyer engagement and financial savings, leveraging WWB’s women-centered design methodology. On this weblog, we share 5 design rules which might be efficient in rising product consciousness, account acquisition and activation amongst Cambodian younger adults (YA).

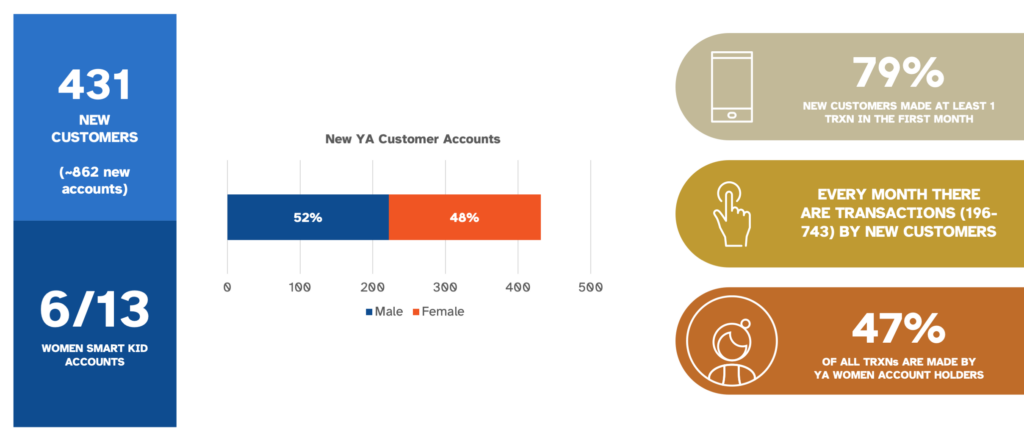

These 5 guiding rules led to 431 new YA prospects (ages 18-35) between February-Could 2023, with 79% of recent prospects making at the least one transaction within the first month. Of those new prospects, 48% (209) have been feminine prospects. With our methodology, we proceed to see product adoption charges on common are the identical for women and men, whereas with out this technique girls prospects are usually left behind.

Pilot Outcomes and Analysis: Elevated Consciousness and Engagement

Our earlier buyer analysis has knowledgeable us that monetary literacy and capabilities amongst low-income Cambodian younger adults are low. Nonetheless, there’s a demand for elevated digital literacy, accessible, and reliable digital monetary providers.

On account of these learnings, we piloted our monetary options between February-Could 2023 and focused non-student YA and YA College college students between the ages of 18 and 35.

The general pilot reached a complete of 71,144 younger adults by means of on-line (digital advertising and marketing through Fb) and offline (on-site sales space activation at universities) campaigns and engagement actions, of which 431 new prospects opened an AMK account, with 79% of recent prospects making at the least one transaction within the first month. Of those new prospects, 48% (209) have been feminine prospects.

The 5 Design Ideas that Led to 431 New AMK Clients

Primarily based on prior buyer analysis, we created answer parts that targeted on elevating buyer consciousness by means of campaigns, learn-by-doing approaches to construct digital monetary capabilities, and incentives to assist construct monetary behaviors and inspire prospects.

These parts boiled down to 5 core design rules. With these rules, we search to assist monetary service suppliers attain out to YA girls prospects and supply them with accessible digital monetary options.

1. Increate total visibility and model

The general pilot reached a complete of 71,144 younger adults by means of on-line (digital advertising and marketing) and offline (on-site sales space activation at universities) campaigns and engagement actions, rising model consciousness amongst YA, particularly YA girls. Leveraging channels that YA choose and use, reminiscent of Fb, YouTube, and Instagram, might help attain the appropriate viewers and assist them make knowledgeable choices on what monetary services and products can be found to them. Via the social media campaigns alone, we reached 35,958 girls prospects by means of static and video posts on Fb.

2. Present Clear worth proposition

For monetary establishments who haven’t served YA girls segments beforehand, there’s a have to re-position themselves to achieve these prospects. It requires speaking its advantages and values that talk to the potential youthful prospects. We took an lively strategy by organising college cubicles to introduce AMK as a reliable monetary supplier, the place YA college students may study extra about AMK and concerning the financial savings account focused in the direction of them.

“I wished to have a separate account for my financial savings. I additionally observed that AMK provides Loyalty Factors on prime of a excessive rate of interest. So, I feel it’s a good match and relevant for college students to avoid wasting up.” – 24-year-old Kampung Cham Province feminine scholar

3. Guarantee easy accessibility and usefulness of digital accounts

YA are usually extra tech-savvy and sometimes choose to transact digitally. Making certain a simple and accessible transaction expertise is taken into account a top-of-funnel aim. Our answer offered straightforward cash-in and cash-out factors that helped prospects fund their digital accounts and actively use, whereas additionally guaranteeing prospects may retrieve their cash when wanted. That is essential for scholar cashflow and desires, particularly for varsity charges, provides, and each day wants.

4. Be taught-by-doing session

In-person assist is confirmed efficient in buying new prospects. Different useful instruments are video tutorials to coach new prospects about merchandise, use them, and may promote wholesome monetary habits. Our answer offered each in-person studying periods together with video tutorials obtainable straight through the cellular banking utility. We see that YA are extra tech-savvy and sometimes in a position to navigate and like studying by themselves. Offering accessible studying tutorials assist support of their curiosity to discover extra digital use instances.

5. Construct digital monetary capabilities

Given the prevalence of digital banking, the answer helped YA girls acquire confidence in utilizing cellular banking for top-ups and transfers. We used a number of channels to remind and inspire prospects, reminiscent of Fb posts and push-notifications conveying messages which might be related to their wants to make use of their cellular banking app.

As core buyer bases start to age, as in AMK’s case, understanding the wants, challenges, and alternatives of serving YA, particularly YA girls prospects, will probably be an necessary step to make sure that also they are financially included. Whereas low-income YA girls prospects face related challenges with digital and monetary literacy and abilities, our learnings and design rules present a pathway in the direction of creating sustainable merchandise and methods to achieve, educate, and assist younger grownup girls prospects use digital monetary providers and merchandise. If monetary service suppliers can present monetary providers, reminiscent of financial savings, for YA earlier than they attain maturity, they will domesticate a brand new technology of financially included, knowledgeable and empowered prospects who can higher plan for and put money into their futures. On the enterprise aspect, monetary service suppliers have the chance to be the financial institution of alternative for this buyer over their lifetime.

This work has been made doable because of funding assist from the Australian Authorities’s Division of International Affairs and Commerce (DFAT).

{kind=link}