What’s in My Mannequin Portfolio is a brand new collection during which chief funding officers and analysts from prime RIAs within the wealth administration trade element their investments and asset allocation in shopper portfolios.

Sequoia Monetary Group, which was based in 1991, has an extended historical past of serving entrepreneurial purchasers all through the lifecycle of their wealth. The RIA has grown to over $15 billion in property, and it not too long ago launched a household workplace division, known as Sequoia Sentinel, to offer extra specialised providers to its ultra-high-net-worth purchasers,

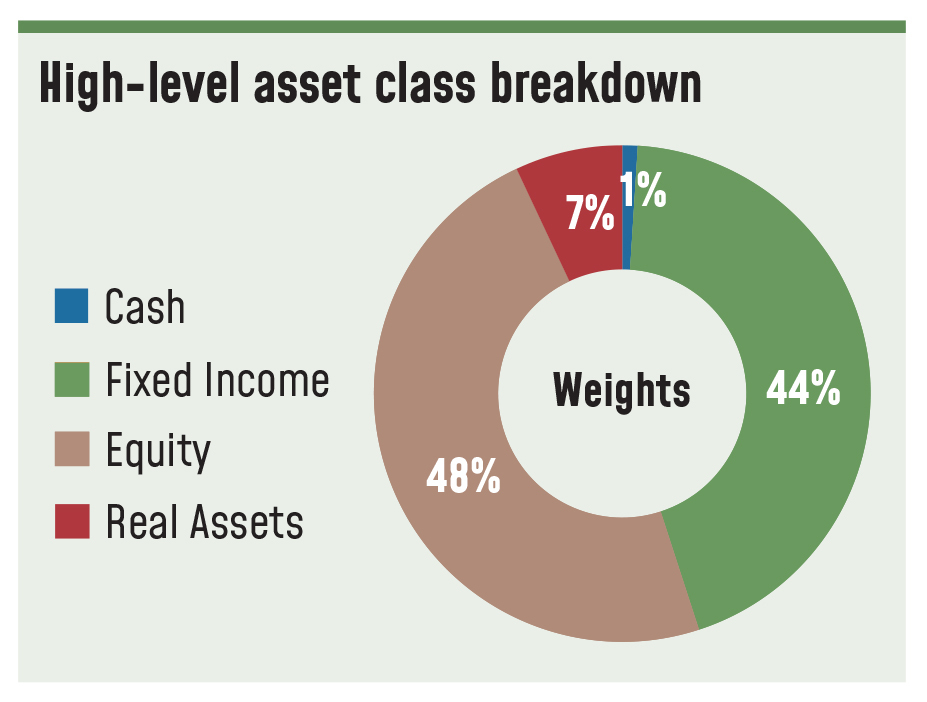

WealthManagement.com spoke with Nick Zamparelli, senior vice chairman, chief funding officer, Sequoia Monetary Group, who supplies a glance inside one of many RIA’s mannequin portfolios, which features a 36% allocation to alternate options.

WealthManagement.com: What’s in your mannequin portfolio?

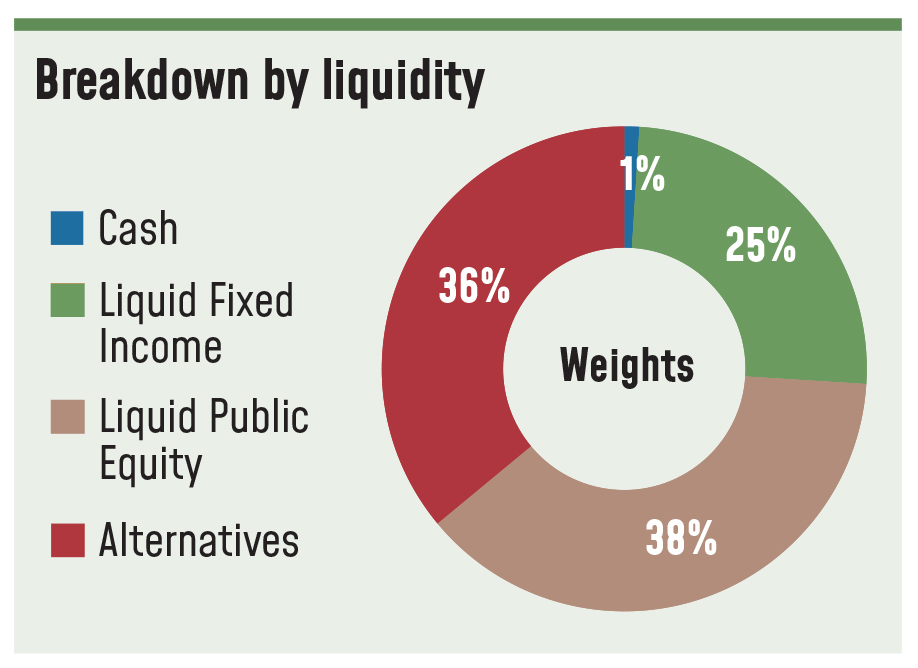

Nick Zamparelli: That is our 50/50 proxy mannequin. At a excessive stage, it contains money, fastened earnings (44%), fairness (48%), some actual property at 7%. However in case you break it out by liquidity, what you will see is that solely 25% is liquid fastened earnings. Solely 38% is liquid public fairness and 36% is alts. After which inside alts, I’ve it damaged out by non-public credit score, non-public fairness, hedge funds and actual property. We’re actually doing a very good job mixing in these illiquid asset courses, and that is actually the place we generate outsized risk-adjusted returns.

Nick Zamparelli: That is our 50/50 proxy mannequin. At a excessive stage, it contains money, fastened earnings (44%), fairness (48%), some actual property at 7%. However in case you break it out by liquidity, what you will see is that solely 25% is liquid fastened earnings. Solely 38% is liquid public fairness and 36% is alts. After which inside alts, I’ve it damaged out by non-public credit score, non-public fairness, hedge funds and actual property. We’re actually doing a very good job mixing in these illiquid asset courses, and that is actually the place we generate outsized risk-adjusted returns.

The Sequoia Sentinel, Sequoia’s household workplace division, shopper has the posh of affording a fabric quantity of illiquidity of their portfolio of property. It is nice for me as an asset allocator as a result of it actually opens up our universe of funding alternatives into alts, into illiquid property. It permits us to essentially exit and search the most effective risk-adjusted returns and seize illiquidity premiums and simply be actually considerate about how we’re constructing out their funding portfolios. The general aim clearly is to construct out considerate portfolio of property in essentially the most opportunistic manner doable.

We use our personal set of capital market assumptions, which is one factor that actually differentiates us, significantly within the non-public house. Personal fairness screens nice in optimizers as a result of the usual deviation of returns seems artificially low merely as a result of it would not get marked as a lot. So, it appears to be like such as you’re producing higher than common fairness—higher than a public fairness returns at a decrease stage of threat, which everyone knows as buyers isn’t true.

So, we make some changes in our mannequin, significantly on commonplace deviation to point out that there’s in actual fact extra threat in non-public fairness than public fairness, for instance. However we provide you with our commonplace set of capital market assumptions that we overview on an annual foundation.

WM: Have you ever made any massive funding allocation adjustments within the final six months or so?

NZ: For, maybe, the primary time in my profession essentially the most contentious conversations inside the analysis staff and admittedly with purchasers are taking place in what must be the chance mitigating section of the portfolio. All the attention-grabbing conversations are happening within the fastened earnings section of the portfolio. So, to that finish, the query actually for the final 18 months is, when to begin leaning into period inside your fastened earnings section, when to tackle a bit bit extra rate of interest threat?

Plenty of of us have been very early—and understandably so given most would have thought that the financial system would have been extra delicate to the climbing cycle than it has turned out to be. Now, there’s plenty of the reason why that is the case, and I believe it was ignored by many market individuals that each shoppers and companies have been in a position to time period out their debt at actually, actually low charges for a very long time.

So, this speedy improve that we noticed on Fed funds actually did not have an effect on their lives but. Now the query will turn into simply how for much longer. The Fed talks about lagged and variable results of rate of interest hikes. All of that stuff continues to be seeping into the financial system. And there’ll come a time when each shoppers and companies must refinance their debt. And in the event that they needed to do it immediately—which they do not, fortunately—then you definately would see that financial sensitivity that individuals have been anxious about. However we have not seen it but.

So, the most important change we have remodeled the previous six months is leaning into period of bid as charges have backed up.

I am attempting to determine a ballast within the portfolio from a threat perspective that offsets my return in search of property, my fairness threat, if you’ll. And the place charges are immediately, I believe you possibly can lastly say that, hey, if we actually get a contraction within the financial system, that fastened earnings immediately goes to assist offset a few of that fairness threat as a result of charges will are available and so they’ll are available fairly aggressively. Everybody’s ready for charges to return down, but when they arrive down for the flawed causes, it is not a very good factor for the fairness market. So, in the event that they’re coming down as a result of there are actual financial issues, it is not going to be favorable to equities as a result of, whereas multiples might profit, the denominator actually isn’t going to profit.

I am attempting to determine a ballast within the portfolio from a threat perspective that offsets my return in search of property, my fairness threat, if you’ll. And the place charges are immediately, I believe you possibly can lastly say that, hey, if we actually get a contraction within the financial system, that fastened earnings immediately goes to assist offset a few of that fairness threat as a result of charges will are available and so they’ll are available fairly aggressively. Everybody’s ready for charges to return down, but when they arrive down for the flawed causes, it is not a very good factor for the fairness market. So, in the event that they’re coming down as a result of there are actual financial issues, it is not going to be favorable to equities as a result of, whereas multiples might profit, the denominator actually isn’t going to profit.

WM: Have you ever made any adjustments on the fairness aspect?

NZ: We have added some quick publicity to our fairness guide. We did that round April or Could. We’re not betting that the market goes down, however we wish to take a number of the volatility out of the potential adjustments in fairness markets. It is turned out to be an actual profit to the portfolio as a result of it served the aim of tamping down the volatility of our fairness returns.

WM: What differentiates your portfolio?

NZ: The analysis course of, in and of itself, actually differentiates us from our rivals. If we’re in search of publicity to a sure asset class, I’ve received seasoned professionals which can be material specialists that may actually discover the most effective methods to articulate these desired exposures. And these guys have a Rolodex. They are not out doing a contemporary search each time. They have sufficient expertise of their space of experience the place they have a bench, they have a roster, they have a Rolodex to select from.

WM: What are your prime contrarian picks?

NZ: One is small cap shares. Have they underperformed and for a very good motive. With the speed atmosphere that we’re in, plenty of small cap shares, the iShares Russell 2000 Worth ETF (IWM) for instance, is riddled with firms which have lower than stellar stability sheets and have to entry the capital markets to fund their progress. And so they cannot do it on this atmosphere. That mentioned, it is an space of progress that we actually need publicity to, and we’re very cognizant of the truth that over lengthy intervals of time, small cap shares have outperformed. In order that’s an space that we’re trying to lean into proper now.

Worldwide fairness is one other space of the market that has underperformed for 15 to 16 years now. After we begin to see progress alternatives broaden out globally, you are going to see a possibility for worldwide shares and rising markets to essentially begin to outperform. You additionally will get a profit if we ever see the greenback weaken. That might be a giant advantage of proudly owning worldwide equities and rising market equities. We’re additionally beginning to take a look at some bond proxy fairness sectors which have simply been decimated.

WM: What funding automobiles do you employ?

NZ: We’ll go from passive to very, very lively. We’ll use passive ETFs the place we do not assume the market is inefficient sufficient to pay for lively administration. For instance, we are going to attempt to make use of passive tax advantaged methods to get our U.S. giant cap publicity, which is a really environment friendly market and really troublesome for lively managers to outperform, significantly given the focus in that house. However within the areas the place it is much less environment friendly—worldwide markets, rising markets, small caps—we are going to exit and discover who we predict are the most effective technique managers. So, we’ll use ETFs, we’ll use mutual funds, we’ll use non-public partnerships.

NZ: We’ll go from passive to very, very lively. We’ll use passive ETFs the place we do not assume the market is inefficient sufficient to pay for lively administration. For instance, we are going to attempt to make use of passive tax advantaged methods to get our U.S. giant cap publicity, which is a really environment friendly market and really troublesome for lively managers to outperform, significantly given the focus in that house. However within the areas the place it is much less environment friendly—worldwide markets, rising markets, small caps—we are going to exit and discover who we predict are the most effective technique managers. So, we’ll use ETFs, we’ll use mutual funds, we’ll use non-public partnerships.

We’ve got our personal inside partnerships that we have created to get publicity to plenty of illiquid asset courses. We’ve got our personal technique known as Area of interest Credit score, which is in non-traditional areas of fastened earnings, like dislocation funds, distressed funds, extra opportunistic areas of the market that transcend simply merely selecting excessive yield, for instance. And on the non-public fairness aspect, now we have a collection of classic funds. We’ll discover methods throughout the spectrum of enterprise all the best way to late stage buyout. A few of these are accredited funds, some are Certified Purchaser funds. Most of our purchasers within the household workplace are QPs.

WM: What are the alternatives you see in actual property proper now? Are there any explicit segments that you are going after or constructions you’re utilizing?

NZ: In non-public markets, we really exit and purchase direct offers. So we personal some business workplace buildings in suburban Philadelphia. We personal some scholar housing tasks—one at Penn State, one at College of Delaware, one on the College of Alabama. Our scholar housing portfolio is performing very, very effectively. Our business workplace is struggling a bit.

We discovered that by proudly owning and working particular person actual property property, we might generate a reasonably wholesome yield for our purchasers. And reasonably than underwriting the credit score high quality of an organization in fastened earnings, you are actually underwriting the credit score high quality of the tenant and the intentions of the tenant.

We’ll use on occasion actual property funds. For instance, we have invested in an industrial actual property fund the place it was simply industrial and warehouse actual property house.

And we additionally will use public REITs. Proper now I might recommend that public REITs, which have already discounted the values of the underlying property through the general public markets, could also be extra attention-grabbing methods, at the very least tactically, to get publicity to actual property than what you are able to do within the non-public markets. It’s actually troublesome on this financing atmosphere to get an actual property deal to pencil out while you’re taking up debt at these ranges. It has been very, very troublesome so as to add new direct actual property alternatives to the portfolio. There might be misery, and now we have capital to deploy. So, we might be opportunistic there for positive.

WM: How are you addressing the inflationary atmosphere inside the portfolio?

NZ: Equities is usually a actual hedge in opposition to inflation. Proper now, if we’re anxious about something, we’re anxious in regards to the shopper. The patron in our view, from what we will see for the true time information that we’re listening to from firms, is getting extra discerning, and the extra discerning they get, the tougher it will be for firms to cross by means of pricing. The tougher it’s for firms to cross by means of pricing, the extra they run into margin points. So, you throw that margin headwind up in opposition to rates of interest and swiftly you have received a possible for earnings to underperform versus estimates.

WM.com: How a lot are you holding in money and why?

NZ: For us, there are two causes to carry money: One is frictional only for shopper bills, which usually is 1% on a regular basis, not a fabric quantity. Or, we might use it as a tactical allocation inside our fastened earnings portfolio. If we have been actually sensible, we’d’ve gone to all money and T-bills firstly of this yr, after which proper round now we’d’ve swapped that into one thing lengthy period. We’ll try this on occasion to handle the period of our fastened earnings portfolio.

WM.com: Are you incorporating ESG into the portfolio? In that case, how?

NZ: ESG has been actually robust for us as a result of it is an space the place we do not essentially belief plenty of the knowledge that we’re getting so far as what makes one thing enticing from an ESG perspective. We have not gotten utterly snug with the info. That mentioned, plenty of our ESG-related investments are shopper pushed. So, when now we have a shopper that has a specific hankering for one thing or they’ve a specific view or they need publicity to one thing or they wish to keep away from one thing, we are going to work with them and discover the most effective methods to try this. We’ll dig in and do some actual diligence to search out them areas the place they’ll be ok with their investments.

{kind=link}